Meet The Bright Future Of Banking: Client-Led Engagement

The greatest opportunity financial institutions have today—bigger than AI, personalization, etc.—is putting customers and members squarely in the driver’s seat of their experience. It’s the key to loyalty, retention, and customer satisfaction (especially when competing with fintechs).

To understand just how powerful allowing clients to take the lead can be, let’s follow the fictional customer Shikha, who’s trying to renew her mortgage:

Shikha stopped by her local institution’s branch on Monday on her lunch break, but the line snaked out the door. Unsure how long she’d have to wait, she headed back to work and went online to see if she could pre-schedule an appointment. This wasn’t an option, so she called the contact center. They told her to visit a branch.

Somewhat irritated, Shikha went in the next day. The line was shorter, but once she got to the front, she learned the mortgage specialist wasn’t in and she would have to return the following week.

Shikha gave herself plenty of time and showed up early on the right day. She finally met with the mortgage specialist. But the paperwork she needed to sign wasn’t ready, and there were additional documents and identification she didn’t know she needed to bring—meaning she’d need to return yet again.

Shikha is being let down—just like so many customers and members across North America. This institution already has her business, and all they’d need to do to keep and expand it is to let her drive. So why is it so difficult for her to engage with them?

The Problem With Banking Journeys Today: Little Choice = Little Convenience

Sadly, Shikha’s story isn’t unique. People can book a vacation across the world online in minutes, but speaking to the right person at a bank or credit union down the street is often harder to arrange.

Why? Because most banks and credit unions have rigid, outdated customer or member journeys and a limited number of connected engagement channels for clients to use. This is so they can control how, when, and where their clients can interact with them—usually by herding customers and members toward a few ineffective, slow-moving channels: their branch or their contact center.

We call this model—still the standard—an “institution-led” engagement model. Here, the institutions drive and decide.

While this may make operations simpler for the institution, the lack of flexibility, choice, and convenience is pushing millions of customers and members like Shikha away. Possibly, into the arms of more modern institutions or fintechs.

Why Institutions Should Shift From Institution-Led Engagement To Client-Led Engagement

Institution led-engagement models leave clients at the mercy of unpredictable wait times, confusing journeys, endless back and forths, and mandatory in-person meetings. It’s a hard pill to swallow when so many other industries offer instant, friendly, self-serve access across channels.

To keep up with consumer demands and remain competitive, institutions need to stop forcing customers and members to engage in ways they don’t love. Instead, they should let their clients take the lead and tell them what they want. And what lots of clients want is a client-led engagement model.

In a client-led journey, customers and members have more convenience and choice when it comes to connecting with your staff and advisors. If you offer many fast, easy, self-serve options across channels, they’ll engage more. And if it’s real-time, they’ll be delighted.

This leads them to purchase their own products, schedule their own appointments, and interact more happily with your staff.

Institution decides

Customer or member decides

Whereas institution-led organizations assume the bank or credit union knows best, a customer-led approach assumes the customer knows best. Because, customers often do.

A customer-led approach allows you to:

- Predict customer or members’ needs—by allowing them to tell you what they need, choose the most convenient channels, and connect with the right person faster.

- Make your team more efficient—with automated, self-serve channels that reduce admin work and streamline meeting and queuing, there’s less busywork and more quality time with clients.

- Staff more appropriately—because when customers book their appointments in advance, traffic is more predictable.

- Generate more business—since customers will see your institution as a way to solve problems, they’ll reach out more often and give it more wallet share.

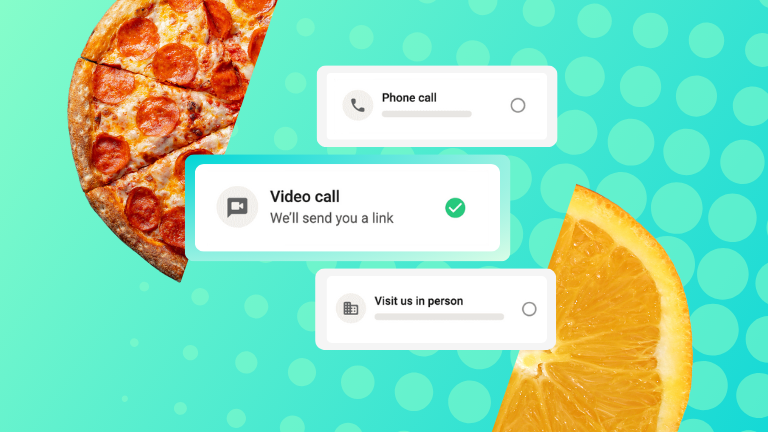

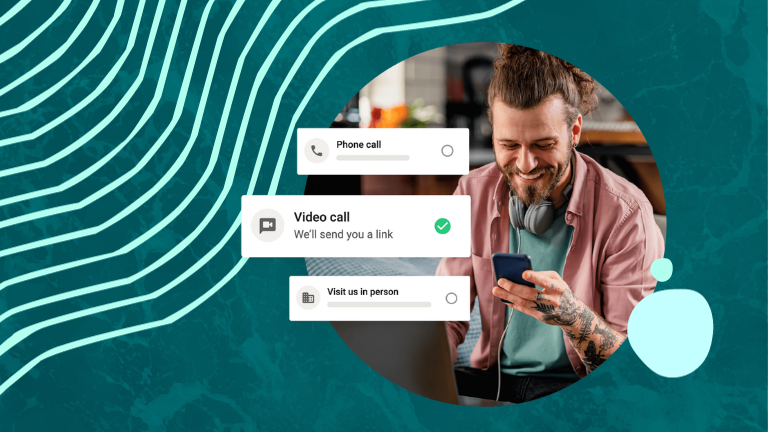

If Shikha banked with a customer-led institution, she would have felt entirely in control of her experience. She could have pre-booked an appointment from their website, skipped the branch visits with a video call, come to her meeting prepared (thanks to pre-appointment reminders and notes), and maybe even have time to discuss other products with her mortgage specialist.

But how can institutions be this flexible? Especially given many are stuck with some legacy systems, little IT support, and staffing challenges? It may not be as cumbersome as you think.

How Financial Institutions Can Let Customers Lead (At Scale)

Customer-led means making it really easy to connect with you. It means taking some of the budget you might otherwise invest in “AI banking” initiatives and reallocating it to simply creating a world-class contact experience. One where customers let you know what they want and when they want it—instead of you trying to predict their next move. (Which institutions are still a long way off from getting right).

Customer-led is also a lot more scalable than institution-led. Rather than forcing everyone into a few unpredictable queues that quickly get backed up (which stresses out staff), it allows customers to find the quickest channel and get help. And it routes many to self-serve options that give them the instant service they need.

You may think offering clients more options to connect will require more complex software, with intelligent routing, a predictive engine, and more customer preference data. And it may also sound like it requires a whole lot of additional resources to run.

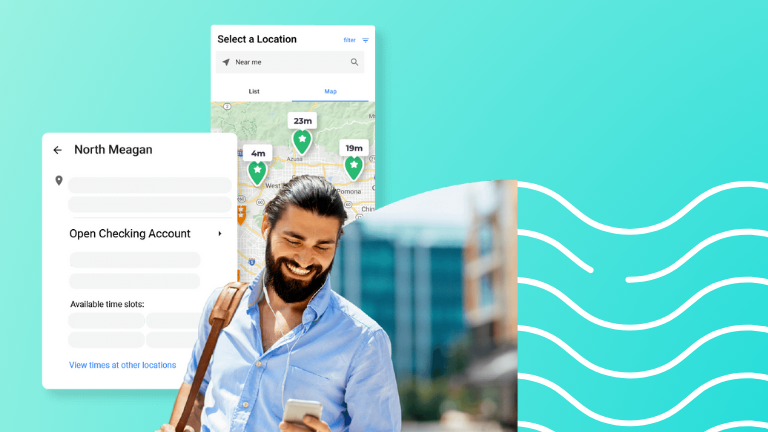

But actually, there are straightforward point solutions built just for this purpose. And they’re fairly easy to implement. For example, an all-in-one appointment and queue management software manages one global queue—whether on the phone, online, or in a lobby—and provides convenient, self-serve options for meeting virtually or in-branch.

And all it takes to get started is an integration with your team’s calendars. This makes it easy for them to see who’s coming in—they know when and why, so it’s easy to prepare for their client’s needs.

And since they spend less time going back and forth to book a meeting, or get context, they spend more quality time with customers and members. They’ll get to ask more important questions. Maybe they’ll be seen more as an advisor, not just a transactional service provider.

The Fix For Today’s Banking Journeys: Customer- or Member-Led Experiences

Introducing tools that reduce friction in the customer or member journey to connect with you is the fastest, simplest way for banks and credit unions to drastically improve the customer and member experience—all by doing less pushing and herding and giving clients simple pathways to (happily) come to them.

And when it’s easier to connect with you, clients do it more often, which leads to more opportunities for new business.

It’s all possible. You just have to open up the traditional queues and channels and let clients have a choice.