Product

A modern way to create human engagement

Why Coconut?

Find out what makes Coconut different

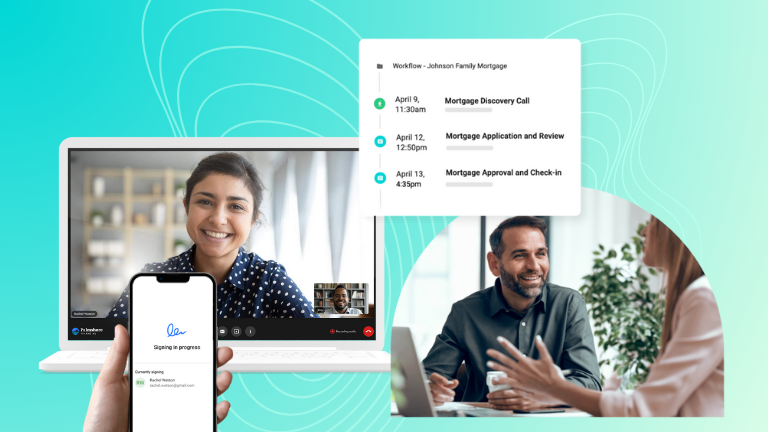

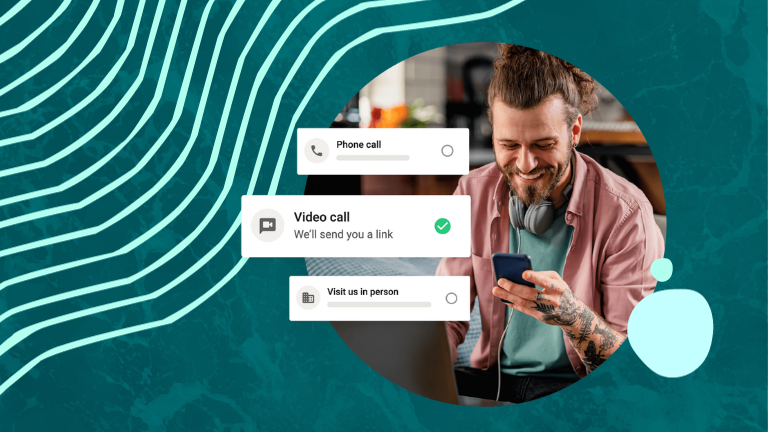

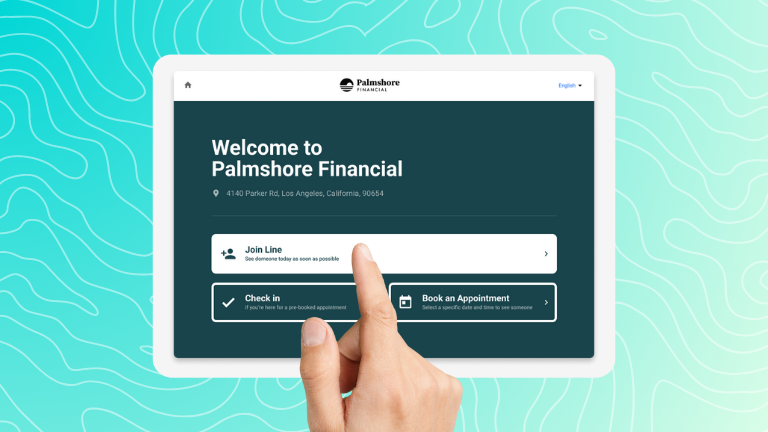

Appointment Scheduling

Provide an effortless experience that goes beyond the appointment.

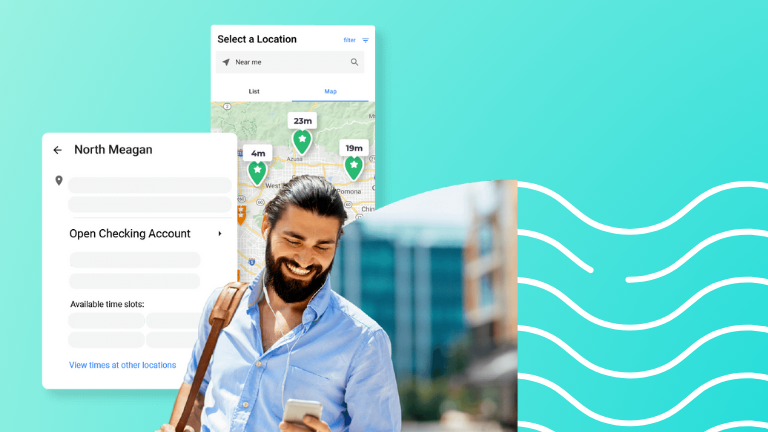

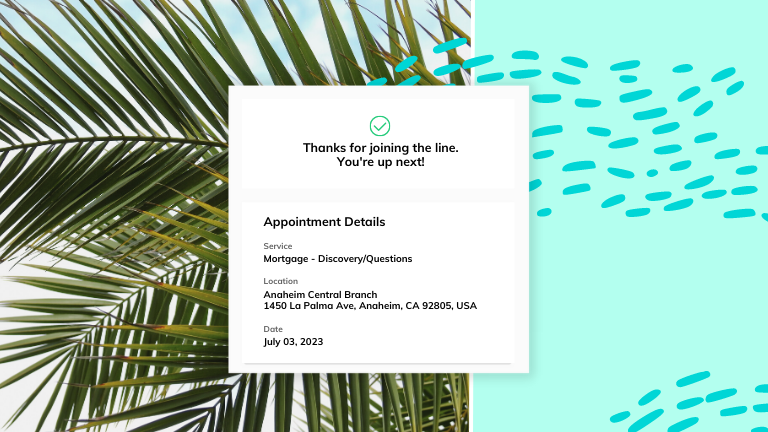

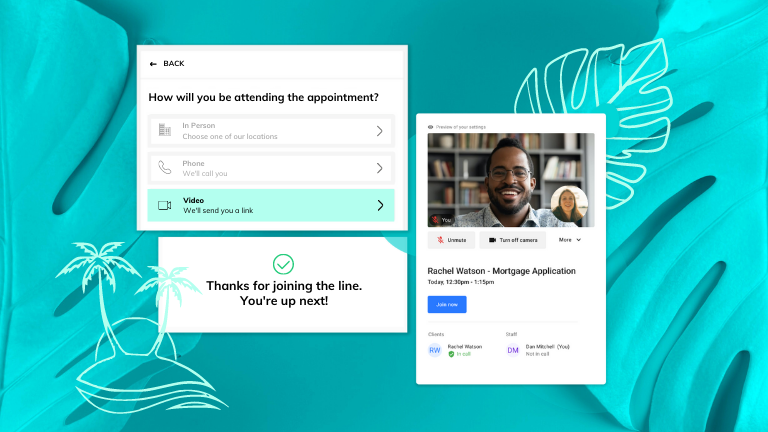

Queue Management

A smarter lobby for a streamlined in-branch experience.

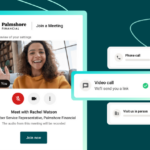

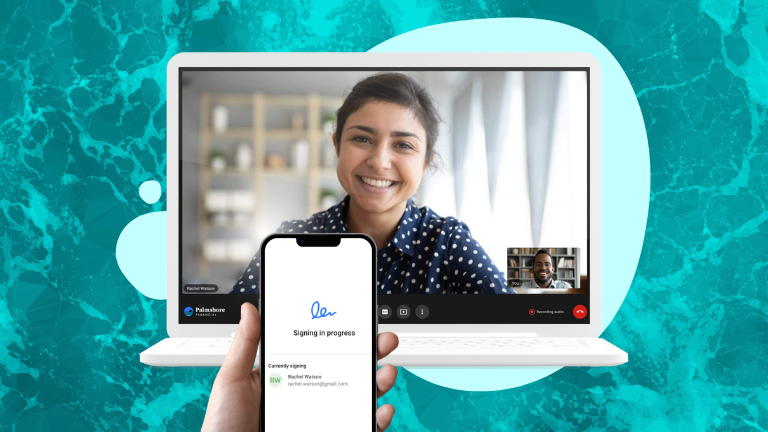

Video Banking

Everything your staff need to deliver an end-to-end video appointment

Reporting & Analytics

See the big picture, and turn insights into action.

Integrations & APIs

We’re flexible to fit where you need us.

Pricing

Solutions

See how Coconut can help your team

Operations

Customer & Member Experience

Marketing

Lending

Resources

Everything you need to make an informed decision

Resource Library

Industry tools, detailed reports, informative webinars, and product information.

Blog

The latest industry trends, product updates, and news, hot off the press.

Success Stories

Learn how our customers have elevated their business with Coconut Software.

Events

Meet the Coconut team (and see Coconut in action) at upcoming events.

Company

Creating meaningful connections since 2007

About

Allow us to introduce ourselves.

Leadership

Meet our inspirational team of thought leaders.

Coconut News

Read all about what’s happening at Coconut.

Careers

Fast-track your career. We’re hiring across teams.

Contact Us

How can we help?

Subscribe

Watch Demo

Speak to an Expert

Open Roles

Login

Blog

Featured

Technology & Transformation

8 Signs It’s Time To Replace Your Appointment Scheduling Software

By Katherine Regnier • Jan 25, 2024

Technology & Transformation

What Does The Branch of the Future Look Like? 8 Trends To Embrace Today

By Katherine Regnier • Jan 18, 2024

Reporting & Data

3 Golden Insights On Balancing Digital & Physical Channels (From A Branch Ops Pro)

By Katherine Regnier • Nov 28, 2023

Reporting & Data

10 Bank Performance Metrics Every Financial Institution Needs To Track

By Katherine Regnier • Nov 22, 2023

Recent

Coconut News

Coconut Software Welcomes Brady Murphy as Chief Revenue Officer

By Coconut Software • Apr 5, 2024

Technology & Transformation

3 Banking Technology Trends Every Bank and Credit Union Needs To Know In 2024

By Katherine Regnier • Jan 11, 2024

Customer & Member Experience

Hybrid Banking Examples: 6 Real Stories From High Growth Banks & Credit Unions

By Katherine Regnier • Nov 14, 2023

Coconut News

Coconut Software Awarded Win in 2023 Technology Fast 50™

By Coconut Software • Nov 8, 2023

Customer & Member Experience

What is Hybrid Banking And How Can You Master It? Everything You Need to Know in 2024

By Katherine Regnier • Nov 7, 2023

All Posts

Coconut Software Announces Integration with Q2’s Digital Banking Platform

By Coconut Software • Oct 16, 2023

Employee Efficiency & Engagement

Operational Efficiency in Banking:

3 Foolproof Strategies Every FI Needs To Know

By Katherine Regnier • Oct 13, 2023

All Posts

How To Solve For Dreaded Staff Shortages In Banks

By Katherine Regnier • Oct 12, 2023

Customer & Member Experience

Customer Experience in Banking: Top Trends to Drive Growth

By Christine Matu • Jun 28, 2023

Technology & Transformation

Banking Queue Management System Guide: FAQs and Evaluation

By Christine Matu • Jun 1, 2023

Employee Efficiency & Engagement

How To Reduce Queues in Banks: 12 Key Techniques, Tips, and Tools

By Christine Matu • May 25, 2023

Technology & Transformation

Queue Management in Banks: The Top Trends and Tools to Know

By Christine Matu • May 18, 2023

Technology & Transformation

Video Banking Services: What To Offer and How To Take it to the Next Level

By Christine Matu • May 11, 2023

Technology & Transformation

What Is Video Banking Software?

By Christine Matu • May 3, 2023

Technology & Transformation

The Top Benefits of Mobile Video Banking

By Christine Matu • Apr 27, 2023

Next

Stay in the loop

Sign up for inspiring stories, helpful resources, and product news.