Hybrid Banking Examples: 6 Real Stories From High Growth Banks & Credit Unions

Today’s financial institutions are adopting digital banking tools at rapid pace, but hybrid banking is still the gold standard for satisfying customer and member needs. Case in point: 78% of Americans say they prefer to bank via mobile app or website, while a significant portion of adults in the U.S. say they prefer to bank in person (29%). In fact, younger generations are even more likely to prefer a combination of digital and in-person banking, and 82% of all consumers say that having a branch nearby is “extremely or very important.”

Clearly, digital banking and traditional brick-and-mortar banking still play a key role in the world of modern financial services. So how can financial institutions (FIs) bridge the gap between the two models? By learning from the industry’s top hybrid banking examples.

A Brief Refresher On Hybrid Banking

Hybrid banking combines the best of both worlds, offering customers the convenience of online banking while maintaining access to physical branches. This approach caters to a diverse customer base and fosters financial inclusivity, accommodating both those who may not have easy access to digital banking tools and those who have challenges around in-person appointments. It puts customers at the helm of their banking experience and gives banks the opportunity to better serve their customers.

But hybrid banking doesn’t just benefit customers and members. By giving employees a more flexible way to work, hybrid banking is also proven to increase staff well-being, productivity, and retention.

Ultimately, it’s a win-win-win for customers, staff, and financial institutions as a whole.

6 Hybrid Banking Examples: Stories From FIs Nailing The Hybrid Experience

Hybrid banking is the best way for FIs to stay competitive and grow in an unpredictable landscape. But blending traditional in-person services with online options isn’t without its challenges. Banks that adopt this model must invest in user-friendly technology that seamlessly blends physical and digital channels. They must also address cybersecurity concerns, data privacy issues, and budget constraints — all while ensuring a positive, personalized customer experience.

It’s a tall order, but many leading banks and credit unions have cracked the code on overcoming these challenges while also meeting consumer demands for a more customized, multi-channel experience.

These six banks and credit unions are amazing hybrid banking examples, showing how to successfully balance digital and physical channels. As a result, they’re delighting customers, improving the overall banking experience, and accelerating growth.

- Yolo FCU: Reducing Wait Times with Teller Express Lanes

Efficiency and staff optimization are key to enhancing customer satisfaction, loyalty, and financial growth. Yolo FCU proves this by offering members the option to schedule quick online appointments for routine transactions. Teller express lanes allow customers to quickly make withdrawals, deposits, wire transfers, savings bonds, account maintenance, and more.

By booking appointments in advance, members secure their spot in the queue, minimizing wait times upon branch arrival. This also benefits staff members, who get advance notifications and can prepare for member requests and significantly reduce the overall branch visit times.

The success of this initiative is clear, with some members saying they’ll never wait in line again. But Yolo FCU is not alone in adopting this efficient approach. A quarter of financial institutions say that pre-scheduled appointments lead to improved closure rates, shorter lead and wait times, and overall customer satisfaction.

- Arvest Bank: Creating a Convenient, Frictionless Customer Experience

Many banks offer multiple service channels, yet customers have a hard time deciding which option to use in a given circumstance. When they don’t have a clear view of how to quickly get help, they’re left frustrated and overwhelmed.

Arvest Bank solved this problem by implementing appointment scheduling and lobby management software that provides real-time availability of advisors that are best suited to help, along with current wait times at local branches. This gives customers an easier way to decide whether to visit a branch, join a phone queue, or use a self-service solution.

The move offered immediate returns, reducing the average wait time from one hour to 15-20 minutes. The bank logged 47,500 pre-booked appointments and 137,600 within the first year of implementation and achieved a 69% completion rate for appointments. Not only that, it also optimized branch operations and staffing levels and improved efficiency in other departments. Best of all, Arvest Bank has happy customers who remain loyal.

- Teachers Federal Credit Union: Leveraging the Power of Video Banking

Though the lockdowns of the COVID-19 pandemic are behind us, many consumers still want to connect with their bank via video. In fact, 35% of bank customers say they prefer video to a face-to-face meeting. Banks have been slow to respond to this trend, with only 36% of FIs investing in video banking options.

This means that the FIs making the investment have a clear competitive advantage. They give customers the flexibility to meet with an advisor from anywhere, while also giving advisors the work flexibility they crave.

Teachers Federal Credit Union leveraged this trend by offering video banking to its members. But they didn’t stop there—they also created a marketing campaign to tout the benefits of video banking channels. The credit union created an FAQ page specifically for video banking, which helped members better understand how to use the service.

Thanks to their comprehensive implementation, the bank now enjoys an expanded reach and higher conversion rates. One potential member joined a video call by accident, yet still stayed on the call for 30 minutes and ended up taking out an auto loan.

“I don’t believe that would have happened had they not been able to see each other face to face,” said Austin Hopkins, AVP of Premier and Relationship Sales at Teachers Federal Credit Union.

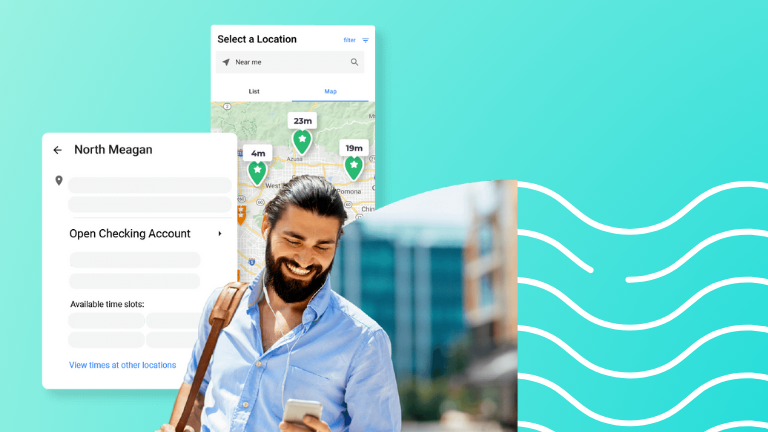

- Credit Union of Southern California: Empowering Customers with Self-Serve Appointment Scheduling

Long wait times don’t just frustrate customers—they also lead to staff burnout, reduced member satisfaction, and loss of potential revenue. Fortunately, queue management tools can change all that, helping to reduce appointment lengths by up to 75%.

Credit Union of Southern California (CU SoCal) experienced these benefits when it adopted self-serve appointment scheduling, which allows customers to pre-schedule appointments with an advisor before they come into the branch. The tool helped customers have a faster, more streamlined way to speak to an advisor and get the help they needed.

As a result, CU SoCal reduced meeting times by 38% and increased loan pull-through rates by 12%. The strategy was so successful that Aaron Young, CU SoCal’s SVP of Retail and Branch Operations said, “We’re increasingly moving walk-ins to high-value appointments and building that behavior because we know appointments convert.”

- US Bank: Providing DIY and “Do It Together” Tools

Today’s customers want options. They may use self-serve tools for simple tasks like withdrawing money or checking a balance, but they also want to engage with advisors for more complex financial conversations. Banks that understand balance will reap the benefits, enjoying greater customer satisfaction, growth, and revenue.

US Bank is one such example of this phenomenon. The FI offers a suite of “do it yourself” and “do it together” tools, which have contributed to their spot at the top of the most prestigious Customer Experience reports.

Since their customers have multiple ways to get things done, they feel empowered and in control of their banking experience. Today, the bank is known for its friendly, easy-to-reach advisors and its innovative approach to hybrid banking. Better yet, the bank enjoyed a 15.55% increase in revenue from 2021 to 2022.

- Navy Federal Credit Union

Banks that value the power of human connection will always have a leg up against those that focus solely on digital processes. For example, Navy Federal Credit Union has stood at the top of Forrester’s Experience Index for the past seven years, in part because the CU is focused on humanizing its digital channels.

“One of our philosophies is that you will always have a path to a human,” said Annie Sebastian, Chief Member Strategy Officer at Navy Federal. “We recognize the importance of that human connection, but with so much interaction happening digitally, we have to … humanize our digital channels.”

The FI does so by conducting surveys, focus groups, and feedback sessions to optimize user experience design and strategy. They strive to understand their members’ needs, and are even considering opening more branches to build on those human relationships.

Reaping the Benefits of Hybrid Banking

Digital banking initiatives are on the rise, with 35% of global banking executives saying they’re focused on digital transformation. Still, a digital-first approach isn’t enough to satisfy ever-changing consumer demands. Digital banking alone can lack the human touch and personal connection members want, and traditional banking alone can lack flexibility and convenience.

In a world where the majority of consumers (86%) value a seamless cross-channel banking experience, a hybrid banking strategy stands out as the best way to increase accessibility and personalization, while also reducing wait times and friction. FIs that embrace the hybrid model are better positioned to compete in the evolving financial industry. They’re able to cater to the diverse needs of customers and stay relevant in an increasingly digital world.

Explore Coconut Software’s self-service banking solutions today to see how we can help your FI successfully adopt the strategies found in these hybrid banking examples. With tools like appointment booking, queue management, video banking, and reporting and insights, we can help your FI seamlessly integrate digital and in-person services, helping to improve client satisfaction, operational efficiency, growth, and retention.