3 Golden Insights On Balancing Digital & Physical Channels (From A Branch Ops Pro)

Besides deposit growth, every financial institution’s experience and operations teams have one thing on their collective hive mind: When do clients want to interact in person, and when would they rather interact with my institution online?

From the delivery of services to transactions to communication, financial institutions have discovered that not all clients want the same combination of physical versus digital. When empathy is the ultimate goal in servicing members, it may seem counterintuitive that robust data, analytics, and interconnected software solutions are the means to get there—but this is exactly what Aaron Young, Senior Vice-President of Branch Operations and Retail Banking at the Credit Union of Southern California, discovered during his FI’s digital transformation.

We asked Jim Marous, podcast host and co-publisher at The Financial Brand, to dig into what Aaron can pass on to other FIs in the midst of their own digital transformations. Watch the full conversation or keep reading for the highlights, with time-stamps to help you dive deeper where you want to.

1. “Digital needs to be an extension of the branch, not the other way around.”

It’s tempting to think digital-first, but Aaron says the reality is that a lot of members may still need education on how something like a mobile app can make their lives easier in the long run.

“One of the things we’re testing right now,” Aaron says, “is when our members come into a branch to open an account, we walk them through our mobile banking app instead of going to a teller.” Aaron notes that people are trained to visit a teller when they need to make a deposit, but that behavior can change with an in-person walkthrough at a branch.

Key phrases Aaron emphasizes are “options” and “what’s possible.” “When we’re thinking about how we can improve the member experience,” he says, “we want to provide options. When you give people options, they’re in control. When you force one direction by only giving one option, that’s where friction starts to happen.”

The Credit Union of Southern California uses data to decide what those options look like. With an understanding that member experience is their only differentiator, they track:

- Member demographics

- Website exits

- Chatbot abandonment

- Coconut online appointment abandonment

- Type of in-branch transactions

- Digital channel paths

Aaron thinks of these data points as breadcrumbs that answer some fundamental questions about his members: Do members leave one channel to go to the next? How many times did they drop off? Why did they drop off? Then, as technology evolves, Aaron connects parts of the digital journey to solve member problems.

2. “Choose platforms that feed data back to pieces of core business.”

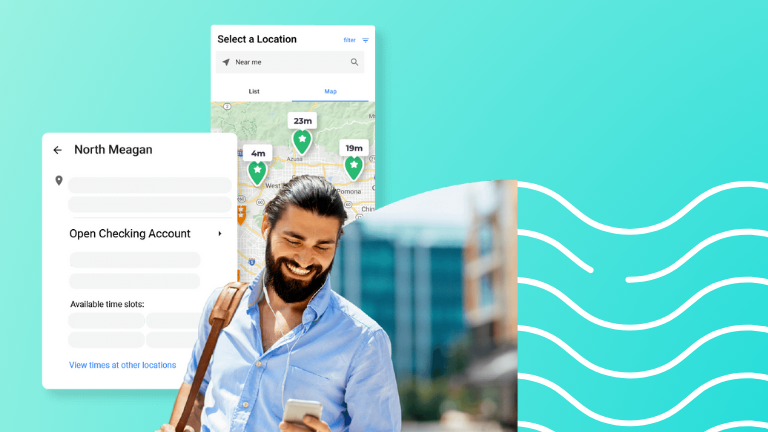

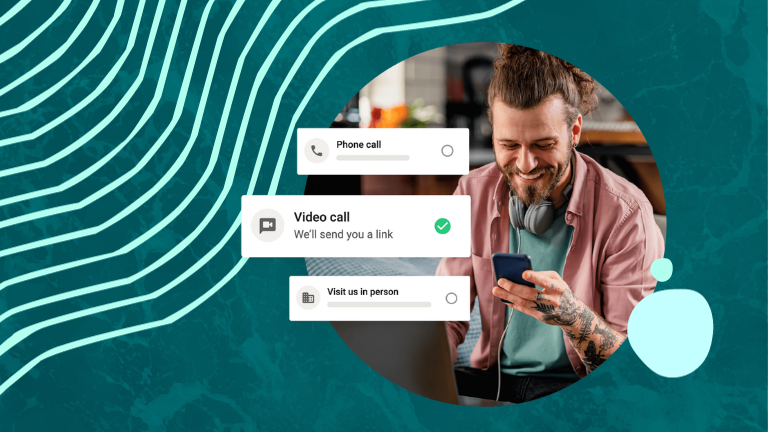

Credit Union of Southern California offers several access points to their members: texting, phone calls, mobile app, chatbots, in-person, video. But Aaron says the institution is ultimately a live answer credit union, and his goal is to make sure he’s giving members the fastest route to completing a task—especially if it means talking to a human being.

“Our phone center is our central nervous system—we aim to answer 75% of our calls in 60 seconds,” Aaron says. “Even when you’re using our chatbot, it’s an easy prompt to speak to a human. We continue to build around that as we grow because we know it’s important for people to be able to get to someone.”

When Aaron started looking for an appointment solution, he prioritized platforms that could increase member satisfaction scores and net promoter scores, both of which increase with human interactions. “We learned through having Coconut in place that our NPS scores are higher when people make an appointment versus when they walk in,” he says. “When members make an appointment, 70% of them give us high scores versus only 30% of walk-ins. When we started out with Coconut and that behavior wasn’t yet built with members, we were getting 600 combined walk-ins and appointments per month. We’re now up to 3,700 combined walk-ins and appointments per month.

3. “Our key to success is transforming into an advice center.”

As financial institutions shift to digital for basic tasks, many of them are repositioning the branch as an advice center that focuses on larger financial challenges. The Credit Union of Southern California is no exception, and a rethinking of their branch locations by type has been as much a part of their digital transformation as technological solutions.

Aaron says this repositioning started with their employees, and he stresses the importance of their involvement from the beginning. “We’ve mapped out the skill sets our team members have today versus what they’ll need as we transition into a more advice-driven model,” he says. “We’re piloting a program for licensed bank employees, and we have a few team members who have volunteered to get insurance training so they can sell annuities.”

Aaron believes that branches still carry major importance, but that modern institutions need to optimize their branch network around their members. “Institutions need to listen to their members and adapt branches to what they need,” he says, “which will determine the style of branch and where they’re located. Credit Union of Southern California is as of now trying to break down the types of branches we have within our configuration.”

While Credit Union of Southern California’s digital transformation isn’t over, Aaron is far enough into the process that he has some thoughts on what he would do differently if he had to start over. Watch his full interview with podcast host Jim Marous and learn how to smooth out your own hybrid model adoption process, make sure your digital and branch transformation journeys work together, and create experiences that make your digital channels feel like an extension of your branch.