Operational Efficiency in Banking:

3 Foolproof Strategies Every FI Needs To Know

A recent survey of more than 150 bank executives found that increasing operational efficiency is the top strategic goal of mid-market banks — and it’s no wonder why. Efficient banks have lower cost-to-income ratios (CIR) and higher return on assets (ROA).

Bank efficiency ratios are one of the most important measures of success in the industry, helping financial institutions (FIs) become more resilient, competitive, and profitable. McKinsey research found that banks that take aggressive measures to improve efficiency can reduce costs by 20 to 40%.

So what can a bank do in order to achieve operational excellence? In this article, we’ll talk more about what operational efficiency means, why it’s crucial, plus we’ll share three proven strategies to increase your bank’s operational efficiency.

What Is Operational Efficiency in Banking?

At its core, operational efficiency is about optimizing the many processes and systems within a bank to maximize productivity and revenue, while also minimizing costs and reducing errors. It encompasses everything from channels, to customers, to staffing, to technology adoption.

This pursuit of efficiency plays a key role in creating a positive customer experience that keeps clients coming back, which in turn, has a huge effect on a bank’s revenue and profit margins.

An efficiently-run bank can process transactions quickly, reduce the likelihood of errors, and offer customers a hassle-free experience, from simple account inquiries to complex financial transactions. It also allows banks to allocate resources more effectively, so they have the means to invest in new technologies, improve customer service, and meet the latest security standards.

3 Reasons Operational Efficiency Should Be A Top Priority For Banks

Why is it important to focus on improving operational efficiency in banks? Because it’s directly tied to customer satisfaction, employee satisfaction, and overall revenue outcomes. Let’s have a look at each in turn.

- Customer Satisfaction

Today’s customers want banks to do more than just open accounts and accept deposits. They want their banks to be active partners in helping them improve every aspect of their financial health. They want personalization, control, and convenience. In fact, one study found that 79% of financial customers will spend more on convenience.

- Employee Satisfaction

When employees have to work on outdated software and deal with broken, inefficient processes, they become overburdened and disengaged. Since just 50% of banking employees are highly engaged and 35% are a retention risk, it is a crucial time for FIs to foster employee engagement and loyalty. It’s incredibly difficult to produce happy customers without happy employees, so employee satisfaction is doubly worth investing in.

- Revenue Outcomes

Happy customers and employees fuel bottomline growth for FIs. According to one recent survey, 92% of consumers say quality customer service is the most important factor when deciding where to open a bank account. Another 63% of consumers say they’re unlikely to leave a bank that offers great customer service, and 78% say they’ll return for similar services. Those satisfied customers are more likely to book appointments, purchase more services, and stick around for the long haul, which has an obvious impact on revenue outcomes.

Ultimately, operational efficiency helps banks meet the ever-evolving expectations of customers and employees, while also helping the institution grow.

3 Tips for Improving Operational Efficiency in Banking

Many FIs see digital transformation as the ultimate path to operational efficiency. And while new technologies certainly can help banks improve overall outcomes, they aren’t the only requirement. In fact, in some cases, use of technology can also introduce new issues, especially if investments in technology make human representatives less available. In fact, customer experience and customer trust have both taken a dip since digital banking became the new normal.

Clearly, banks must take a more well-rounded approach to operational efficiency in 2024. For better results, banks should implement the following three strategies.

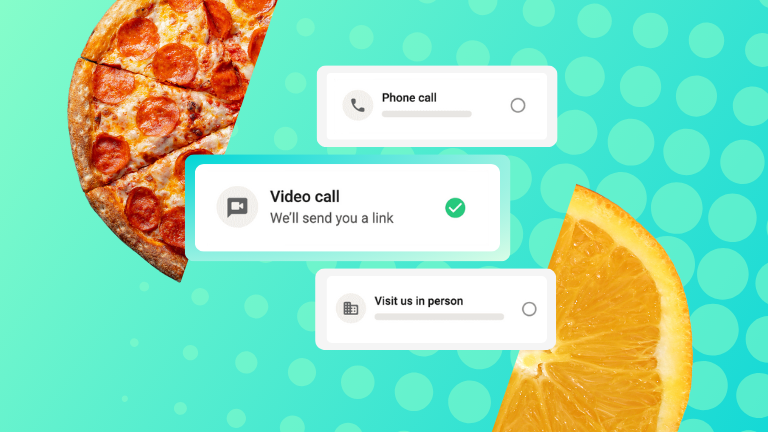

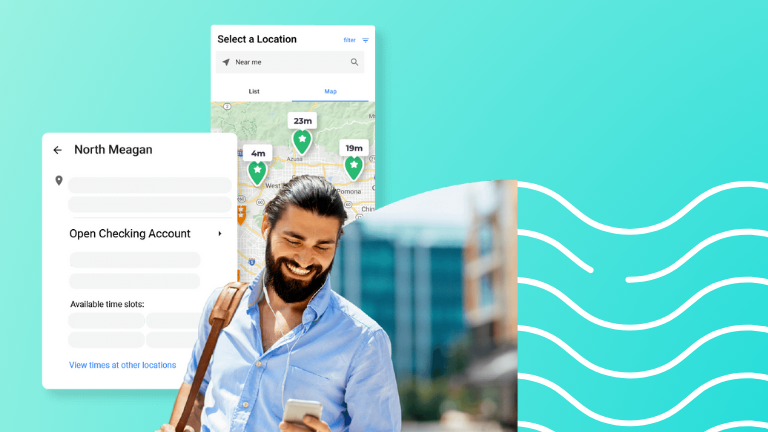

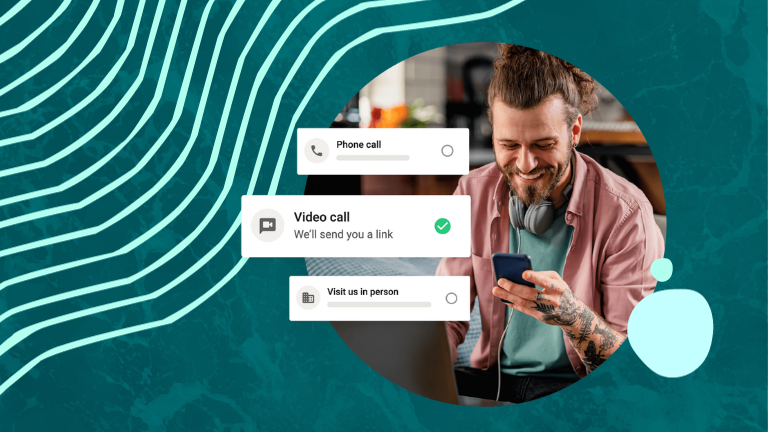

1. Channel Optimization

Digital banking experiences can help streamline many customer activities, but there are still some instances where customers need face-to-face interaction with an advisor. Banking surveys repeatedly find that hybrid experiences outperform digital-only or in-person-only experiences.

On the same note, a recent Deloitte survey found that consumers like using digital channels for transactional activities, but they still prefer visiting a branch for “high-touch interactions” such as:

- Inquiring about new products

- Applying for a loan

- Opening a new checking account

- Opening a new wealth management account

- Receiving financial advice

In short, customers want a mix of in-person and digital experiences, and banks must optimize their channels to find that sweet spot.

Many FIs are taking this approach by treating their branches as “advice centers” — a place where customers can connect with a financial advisor for expert advice. At the same time, they’re investing in video banking services, which allow customers to connect with a financial advisor from anywhere, without wasting time driving to the location. Since 36% of financial customers say they prefer video over meeting in person, this balance plays a critical role in increasing customer satisfaction.

It’s all about connecting customers with the advice they want, when and where they want it. Today’s customers have diverse needs, and banks must optimize channels to serve a variety of preferences.

2. Staff Efficiency

Customers are more likely to remember how they felt about an interaction than to focus on the actual outcome of the interaction. This highlights just how important it is to prioritize employee needs as much as customer needs. After all, a happy employee is more likely to create positive experiences for customers. On the other hand, employees who are overworked and dissatisfied negatively impact the customer experience.

For this reason, the leading FIs aren’t just seeking ways to reduce customer friction — they’re also looking for ways to improve the employee experience.

FIs that prioritize staffing efficiencies are more likely to report:

- High customer satisfaction scores

- Optimism about growth outlooks

- Higher share of wallet

Banks can improve staff efficiency by leveraging technology that saves time, reduces errors, and helps staff better prepare for appointments with customers. For example, bank appointment software can increase visibility across the institution, making it easier for administrators to staff branches, follow up after appointments, and track the effectiveness of current operations.

3. Better Data

There’s no doubt about it — better data leads to better banking experiences for customers, employees, and the institution as a whole. Without accurate insights on hand, banks may not recognize opportunities to improve operational efficiency, and they may struggle to understand customer needs and wants.

This is where data tracking comes into play. The top-performing FIs closely track data related to three categories:

- Customer experience

- Staff performance

- Overall revenue outcomes

As institutions track metrics related to branch traffic volume, appointment volume, lead times, and more, they garner insights that are directly tied to performance across staff and channels. They can then use these insights to become more efficient, deliver a better experience, and improve customer satisfaction scores.

Real Stories Of How Two Banks Improved Their Operational Efficiency

Operational efficiency in banking isn’t just a nice idea — it’s a strategy that’s changing outcomes for financial institutions around the world. Let’s take a look at two case studies that highlight how operational efficiency can drive growth, improve member satisfaction, and increase revenue.

CU SoCal: Turning Walk-Ins Into High-Value Appointments

Credit Union of Southern California (CU SoCal) offers a full suite of products and services for its members, including checking, savings, mortgages, investment services, and more.

When Aaron Young, SVP of Branch Operations and Retail Banking, was seeking ways to improve operational efficiency, he turned to Coconut Software. Aaron and his team selected Coconut’s digital appointment scheduling platform with the goal of turning walk-ins into high-value appointments.

Now when a potential member books an appointment, an advisor reaches out and asks quality questions to really understand their needs. They use Coconut data to develop actionable strategies that improve efficiency, grow membership, and grow loans. Here’s a snapshot of their results:

- Increased loan pull-through ratio from 48% to 60%

- Ranked #1 among 135 credit unions for customer satisfaction

- Decreased appointment length by 38%

- Increased funded loan applications by 12%

Coconut Software helped CU SoCal improve operational efficiency by connecting channels, improving processes and appointment outcomes, and fostering a best-in-class client experience.

Kawartha CU: Using Data to Better Serve Member Needs

Headquartered in Peterborough, Ontario, Kawartha Credit Union strives to improve the financial success and overall well-being of its members and community. The credit union offers values-based financial advice, along with a range of financial solutions and convenient service channels.

In 2018, Kawartha CU found that members were booking appointments, but weren’t always showing up. Sometimes members booked appointments at the wrong location but realized their mistake when it was too late to make it to the correct branch.

The credit union turned to Coconut Software for precise insights that better enabled operational decisions and an easy user experience for both members and staff. As a result, appointment no-shows decreased, the institution has a better view into behaviors and preferences, and they now offer better hours that serve member needs.

Achieving Operational Excellence

The ideal bank efficiency ratio hovers around 50%. Yet even the top 100 banks struggle to reach a ratio below 59%. Is your FI in this camp?

If so, Coconut Software may be the answer. We’ve helped top-performing FIs achieve operational excellence by blending the benefits of in-person and digital banking services. Our easy-to-use software empowers FIs to create seamless personalized experiences that put customers and members in the driver’s seat.

With a suite of tools including appointment scheduling, queue management, and video banking, Coconut helps FIs keep up with customer and employee expectations, save time, make better connections, and grow efficiently. Speak to an expert today to learn why banks and credit unions love Coconut Software.